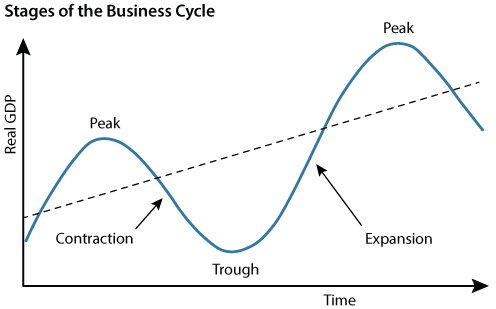

Business Cycle

Business Cycles

Economic theorists in different time periods have attempted to explain and bring out the causative factors of Business Cycles and their initiation. The classical economists, Keynesian economics, and then the new classical models have tried, with their respective assumptions, to bring about a broad explanation of the occurrence of Business Cycles in a general equilibrium or a partial equilibrium framework.

Starting off with the classical model, the main pioneers of explaining this were Milton Friedman, Edmund Phelps and Robert Lucas, who broadly named it “the fooling model”.

According to this model, “information” plays a pivotal role in determining business cycles. It argues that there is asymmetric information in the market, wherein either the workers or the firms, or both do not possess complete information about the prevailing market prices and wage rates. Hence, they tend to overproduce or underproduce based on their expectations which may or may not be realised. These fluctuations sometimes lead the economy to boom and sometimes pushes the economy into recession.

However, in the long run, there is a tendency to move back to the natural level of output at a given natural rate of unemployment. This is because the workers have access to information in the long run. To cite an example, if there’s a sudden increase in the inflation rate leading to a fall in the real wages. However, if the nominal wages are increased by an amount lesser than the inflation rate, the net effect is a fall in real wage. Since there’s asymmetric information on the workers end, they presume this nominal wage increase holding their assumption about inflation constant. Labour supply increases and so does the output, leading to a boom period.(Natural rates of output and unemployment are attained where the market-determined wages and prices are at equilibrium).

Robert Lucas presents the “policy ineffectiveness proposition” which argues that only an unanticipated monetary expansion can lead to a change in output. The monetary authority has to initiate a “price surprise” for real variables to change.

Unrealistic assumptions like continuous market clearing and the argument that “people being fooled” will lead to business cycles seemed baseless and were criticised by other economists.

After the Great Depression of the 1930s, the Keynesian model of Business cycles emerged, explaining the reasons behind the same, naming it “the RBC model”. It takes into account, the idea of rational expectations. Although the assumption of rational expectations may not be entirely correct, it makes use of all the available information and a non-stochastic error term. It assumes the stickiness of wages and prices. It argues that supply-side shocks and nominal rigidities lead to business cycles.

Supply-side shocks: This includes advancements in technology, weather conditions, price fluctuations of raw materials etc. These shocks are highly persistent and for a considerable amount of time for business cycles to occur. Although, this model was criticised on the grounds that retards in technology don’t lead to recession. Also, there are a lot of demand-side factors that determine the emergence of business cycles, not limiting it to the supply-side effects.

Nominal and real Rigidities: High marginal costs, menu costs, shoe-leather cost and other costs of inflation are the reason why nominal prices are rigid and do not change so easily. Wage contracts such as COLA (cost of living agreement) is another factor which makes the real wages rigid. These contracts generally index wages according to inflation such that their real wage remains unchanged or if nit full indexation, ensures that it is unaffected to a certain extent.

Keynesian model too, faced its own share of criticism. For instance, one argument claimed that business cycles prevailed even before labour unions were formed thus disregarding real rigidity as the reason for business cycles.

Later on, the Dynamic Stochastic General Equilibrium was developed which included aspects of the above two models along with more realistic assumptions and taking into account a broader view of the economy and explaining general equilibrium.

Written by Tharuni Mudumby