Price Elasticity of Demand

Written by Amina Meirkhan | Proofread by Yasmin Uzykanova

Subject vocabulary:

Price elasticity of demand (PED) - the responsiveness of demand to a change in price.

Inelastic demand - when the change in the quantity demanded is proportionately smaller than the change in price.

Elastic demand - when the change in the quantity demanded is proportionately greater than the change in price.

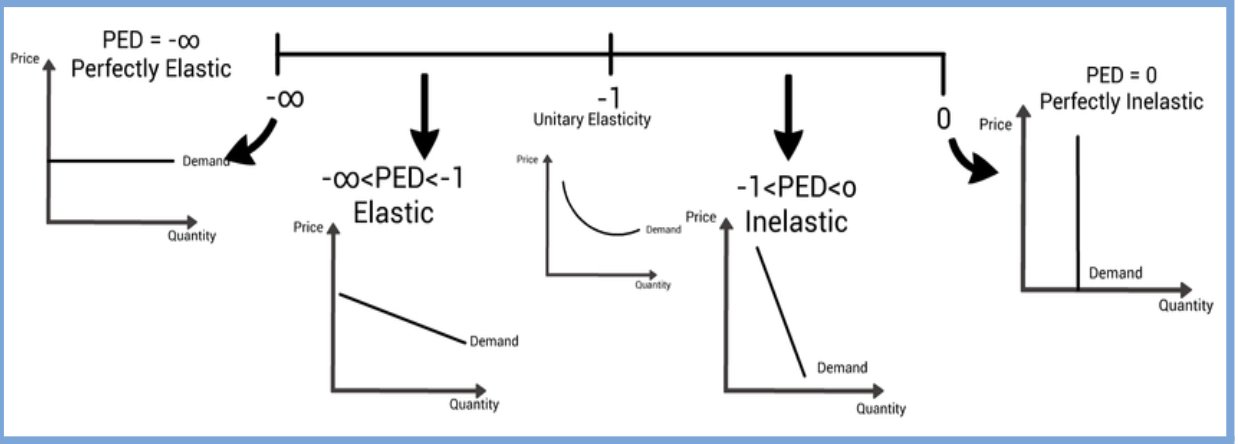

Perfectly elastic demand - when PED is equal to infinity, therefore any increase in price will cause quantity demanded to be 0.

Perfectly inelastic demand - when PED is equal to 0, therefore a change in price will cause no change in quantity demanded.

Unitary elasticity of demand - when PED is equal to -1, therefore the responsiveness of demand is proportionately equal to the change in price.

Substitute - good that is bought as an alternative to another good, but performs the same function.

Formula to calculate PED:

Tip: to remember the formula easier, “you Queue before you Pee”. This helps you to remember that quantity is on the top of the fraction (numerator) and price is on the bottom (denominator).

PED always comes out as a negative value!

PED is inelastic if the value is more than -1, for example -0.5.

PED is elastic if the value is less than -1, for example 2.5.

Graphical representations of PED:

Factors affecting PED:

Availability of substitutes - products with lots of substitutes have elastic demand, because consumers can easily switch from one product to another. Vice versa for products with few or no substitutes.

Degree of necessity - necessities have inelastic demand, because consumers need them and cannot decrease the amount they purchase significantly. Vice versa for non-essential goods like luxuries. In addition, a habit forming product can become a necessity and have inelastic demand.

Proportion of income spent on a product - if consumers spend a big proportion of their income on a product, its demand is more elastic. Vice versa for products that cost very little in relation to income.

Time - in the short term, goods have inelastic demand because it takes time for consumers to find substitutes. Vice versa for the long term.